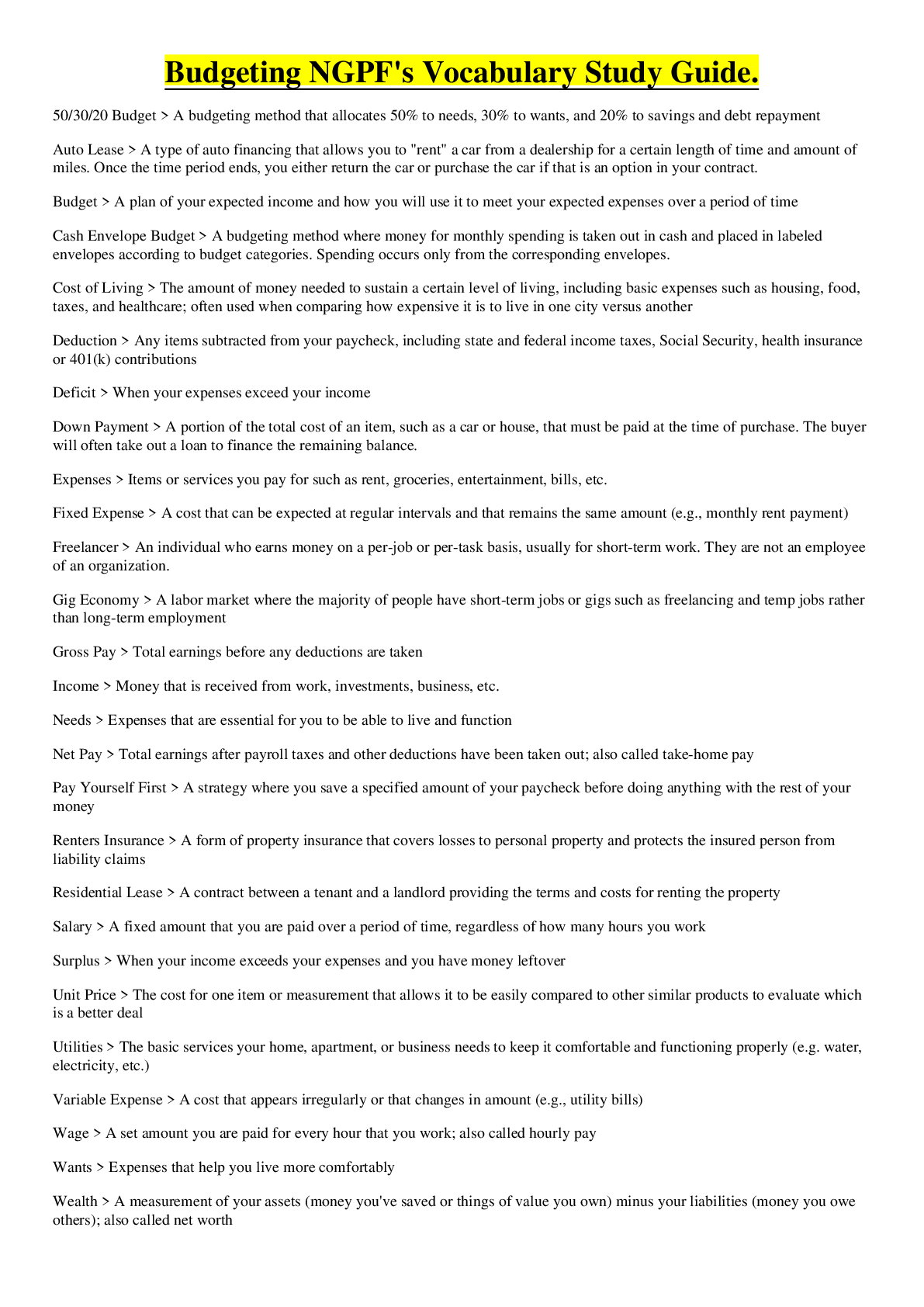

Marketing > STUDY GUIDE > MKT 3210 Exam 3 VOCAB STUDY GUIDE (All)

MKT 3210 Exam 3 VOCAB STUDY GUIDE

Document Content and Description Below

MKT 3210 Exam 3 VOCAB STUDY GUIDE Chapter 8: Attributes – include features, functions, benefits, and uses of a product; marketers view products as a bundle of attributes that includes the pa... ckaging, branding, name, benefits, and supporting features in addition to a physical good Good – a tangible product that we can see, ouch, smell, hear, or taste Core product – all the benefits the product will provide for consumers or business customers Actual product – the physical good or the delivered service that supplies the desired benefit Augmented product – the actual product plus other supporting features such as a warranty, credit, deliver, installation, and repair service after the sale Durable goods – consumer products that provide benefits over a long period of time, such as cars, furniture, and appliances Nondurable goods- consumer products that provide benefits for a short time because they are consumed or are no longer useful Convenience product – a consumer good or service that is usually low prices, widely available, and purchased frequently with a minimum of comparison and effort Staple products – basic or necessary items that are available almost everywhere Consumer packaged good (CPG) – or fast-moving consumer goods (FMCG); a low cost good that is consumer quickly and replaced frequently Impulse products – a product people often buy on the spur of the moment Emergency products – products we purchase when we’re in dire need Shopping products – goods or services for which consumers spend considerable time and effort gathering information and comparing alternatives before making a purchase Specialty products – goods or services that have unique characteristics and are important to the buyer and for which he or she will devote significant effort to acquire Unsought products – goods or services for which a consumer has little awareness or interest until the product or a need for the product is brought to his or her attention Equipment – expensive goods that an organization uses in its daily operations that last for a long time Maintenance, repair, and operating (MRO) products – goods that a business customer consumes in a relatively short time Raw materials – products of the fishing, lumber, agricultural, and mining industries that organizational customers purchase to use in their finished products Processed materials – products created when firms transform raw materials from their original state Specialized services – services that are essential to the operation of an organization but are not part of the production of a product Component parts – manufactured goods or subassemblies of finished items that organizations need to complete their own products Innovation – a product that consumers perceive to be new and different from existing products Creativity – a phenomenon whereby something new and valuable is created Continuous innovation – a modification of an existing product that sets one brand apart from its competitors Knockoff – a new product that copies, with slight modification, the design of an original product Dynamically continuous innovation – a change in an existing product that requires a moderate amount of learning or behavior change Discontinuous innovation – a totally new product that creates major changes in the way we live Convergence – the coming together of two or more technologies to create a new system with greater benefits than its separate parts Research and development (R&D) – a well-defined and systematic approach to how innovation is done within the firm New product development (NPD) – the phases by which firms develop new products, including idea generation, product concept development and screening, marketing strategy development, business analysis, technical development, test marketing, and commercialization Idea generation (ideation) – a phase of product development in which marketers use a variety of sources to come up with great new product ideas that provide customer benefits that are compatible with the company mission Value co-creation – the process by which benefits-based value is created through collaboration participation y customers and other stakeholders in the new product development process Product concept development and screening – the second step of product development in which marketers test product ideas for technical and commercial success Technical success – indicates that a product concept is feasible purely from the standpoint of whether or not it is possible to physically develop it, regardless of whether it is perceived to be commercially viable Commercial success – indicates that a product concept is feasible from the standpoint of whether the firm developing the product believes there is or will be sufficient consumer demand to warrant its development and entry into the market Business analysis – the step in the product development process in which marketers assess a product’s commercial viability Technical development – the step in the product development process in which company engineers refine and perfect a new product Prototypes – test versions of a proposed product Patent – a legal mechanism to prevent competitors from producing or selling an in invention, aimed at reducing or eliminating competition in a market for a period of time Market test – (test market); testing the complete marketing plan In a small geographic are that is similar to the larger market the firm hopes to enter Simulated market test – application of special computer software to imitate the introduction of a product into the marketplace allowing the company to see the likely impact of price cuts and new packaging – or even to determine where in the store it should try to place the product Commercialization – the final step in the product development process in which a new product is launched into the market Crowdfunding – online platforms that allow thousands of individuals to each contribute small amounts of money to find a new product from a startup company Product adoption – the process by which a consumer or business customer begins to buy and use a new good, service, or idea Diffusion – the process by which the use of a product spreads throughout a population Tipping point – in the context of product diffusion, the point when a product’s sales spike from a slow climb to an unprecedented new level Adoption pyramid – reflects how a person goes from being unaware of an innovation through stages from the bottom up of awareness, interest, evaluation, trial, adoption, and confirmation Media blitz – a massive advertising campaign that occurs over a relatively short time frame Impulse purchase – a purchase made without any planning or search effort Beta test – limited release of a product, especially an innovated technology, to allow usage and feedback from a small number of customers who are willing to test the product under normal, everyday conditions of use Bleeding edge technology – an innovation technology that is not yet ready for release to the market as a whole, potentially because of issues related to reliability and stability but is in a suitable state to be offered for beta testing to evaluate consumer perceptions of its performance and identify a potential issues in its usage Innovators – the first segment (roughly 2.5%) of a population to adopt a new product Early adopters – those who adopt an innovation early in the diffusion process but after the innovators Early majority – those whose adoption of a new product signals a general acceptance of the innovation Late majority – the adopters who are willing to try new products when there is little or no risk associated with the purchase, when the purchase becomes an economic necessity, or when there is social pressure to purchase Laggards – the last consumers to adopt an innovation Relative advantage – the degree to which a consumer perceives that a new product provides superior benefits Compatibility – the extent to which a new product is consistent with existing cultural values, customs, and practices Complexity – the degree to which consumers find a new product or its use difficult to understand Trialability – the ease of sampling a new product and its benefits Observability – how visible new product and its benefits are to others who might adopt it Chapter 9: Product management – the systematic and usually team-based approach to coordinating all aspects of a product’s strategy development and execution Product line – a firm’s total product offering designed to satisfy a single need or desire of the target customers Product length – determined by the number of separate items with the same category Stock-keeping unit (SKU) – a unique identifier for each distinct product Cannibalization – the loss of sales of an existing brand when a new item in a product line or product family is introduced Product mix – the total set of all products a firm offers for sale Product mix width – the number of different product lines the firm products Product quality – the overall ability of the product to satisfy customer expectations Total quality management (TQM) – a management philosophy that focuses on satisfying customers through empowering employees to be an active part of continuous quality improvement Internal customers – coworkers that interact who harbor the attitude and belief that all activities ultimately impact external customers Internal customer mind-set – an organizational culture in which all the organization members treat each other as valued customers ISO 9000 – criteria developed by the International Organization for Standardization to regulate product quality in Europe Six Sigma – a process whereby firms work to limit product defects to 3.4 per million or fewer Product life cycle (PLC) – a concept that explains how products go through four distinct stages from birth to death: introduction, growth, maturity, and decline Introduction stage – the first stage of the product life cycle in which slow growth follows the introduction of a new product in the marketplace Growth stage – the second stage in the product life cycle, during which consumers accept the product and sales rapidly increase Maturity stage – the third and longest stage in the product life cycle, during which sales peak and profit margins narrow Decline stage – the final stage in the product life cycle during which sales decrease as customer needs change Brand – a name, term, symbol, or any other unique element of a product that identifies one firm’s product(s) and sets it apart from the competition Trademark – the legal term for a brand name, brand mark, or trade character; trademarks legally registered by a government obtain protection for exclusive use in that country Brand equity – the value of a brand to an organization Brand meaning – the beliefs and associations that a customer has about the brand Brand storytelling – compelling stories told by marketers about brands to engage consumers Brand extensions – a new product sold with the same brand name as a strong existing brand Brand dilution – a reduction in the value of a brand typically driven by the introduction of a brand extension that possesses attributes that adversely contrast with the current attributes consumers associate with the brand Sub-branding – creating a secondary brand within a main brand that can help differentiate a product line to a desired target group Family brand – a brand that a group of individual products or individual brands share National or manufacturer brands – brands that the product manufacturer owns Private-label brands – brands that a certain retailer or distributor owns and sells Generic branding – a strategy in which products are not branded and are sold at the lowest price possible Licensing – an agreement in which one firm sells another firm the right to use a brand name for a specific purpose and for a specific period of time Cobranding – an agreement between two brands to work together to market a new product Ingredient branding – a type of branding in which branded materials become “component parts” of another branded product Package – the covering or container for a product that provides product protection, facilitates product use and storage, and supplies important marketing communication Universal Product Code (UPC) – a set of black bars or lines printed on the side or bottom of most items sold in grocery stores and other mass-merchandising outlets that correspond to a unique 10-digit number Sustainable packaging – packing that involve one or more of the following: elements of the packaging that can be produced from previously used materials, elements of the packaging that use materials in their development that can be repurposed after use, the use of materials that require fewer resources to cultivate, and the use of materials and processes that are generally less harmful to the environment Copycat packaging – packaging designed to mimic the look of a similar or functionally identical national branded product often meant to lead the consumer to perceive the two products as comparable Brand manager – an individual who is responsible for developing and implementing the marketing plan for a single brand Product category managers – individuals who are responsible for developing and implementing the marketing plan for all the brands and products within a product category Market manager – an individual who is responsible for developing and implementing the marketing plans for products sold to a particular customer group Venture teams – groups of people within an organization who work together to focus exclusively on the development of a new productChapter 10 Price – the assignment of value, or the amount the consumer must exchange to receive the offering Bitcoin – the most popular and fastest-growing digital currency Market share – the percentage of the market accounted for by a specific firm, product line, or brand Prestige products – products that have a high price and that appeal to status-conscious consumers Price elasticity of demand – the percentage change in unit sales that results from a percentage change in price Elastic demand – demand in which changes in price have large effects on the amount demanded Inelastic demand – demand in which changes in price have little or no effect on the amount demanded Cross-elasticity of demand – when changes in the price of one product affect the demand for another item Variable costs – the cost of production that are tied to and vary, depending on the number of units produced Fixed costs – costs of production that do not change with the number of units produced Average fixed cost – the fixed cost per unit produced Total costs – the total of the fixed and variable costs for a set number of units produced Break-even analysis – a method for determining the number of units that a firm must produce and sell at a given price to cover all its costs Break-even point – the point at which the total revenue and total costs are equal and beyond which the company makes a profit; below that point, the firm will suffer a loss Contribution per unit – the difference between the price the firm charges for a product and the variable costs Markup – an amount added to the cost of a product to cover the fixed cost of a product to create the price at which a channel member will sell the product Gross margin – the markup amount added to the cost of a product to cover the fixed costs of the retailer or wholesaler and leave an amount for a profit Retailer margin – the margin added to the cost of a product by a retailer Wholesaler margin – the amount added to the cost of a product by a retailer List price or manufacturer’s suggest price (MSRP) – the price that the manufacturer sets as the appropriate price for the end consumer to pay Vertical integration – the combination of manufacturing operations with channels of distribution under a single ownership to reduce costs and increase profits Shopping for control – consumers, facing a world with terrorism and political unrest, value products and services that provide some degree of control, such as installing smart home technology or moving to gated communities Cost-plus pricing – a method of setting prices in which the seller totals all the costs for the product and then adds an amount to arrive at the selling price Keystoning – retail pricing strategy in which the retailer doubles the cost of an item (100% markup) to determine the price Demand-based pricing – a price-setting method based on estimates of demand at different prices Target costing – a process in which firms identify the quality and functionality needed to satisfy customers and what price they are willing to pay before the product is designed; the product is manufactured only I the firm can control costs to meet the required price Yield management pricing – a practice of charging different prices to different customers to manage capacity while maximizing revenues Price leadership – a pricing strategy in which one firm first sets its price and other firms in the industry follow with the same or similar prices Value pricing – (everyday low pricing); a pricing strategy in which a firm sets prices that provide ultimate value to customers High/low pricing – (promo pricing); a retail pricing strategy in which the retailer prices merchandise at list price but runs frequent, often weekly, promotions that heavily discount some products Skimming price – a very high, premium price that a firm charges for its new, highly desirable product Penetration pricing – a pricing strategy in which a firm introduces a new product at a very low price to encourage more customers to purchase it Trial pricing – pricing a new product low for a limited period of time to lower the risk for a customer Price segmentation – the practice of charging different prices to different market segments for the same product Peak load pricing – a pricing plan that sets prices higher during periods with higher demand Surge pricing – a pricing plan that raises prices of a product as demand goes up and lowers it as demand slides Bottom of the pyramid pricing – innovative pricing that will appeal to consumers with the lowest incomes by brands that wish to get a foothold in the bottom of the pyramid countries Two-part pricing – pricing that requires two separate types of payments to purchase the product Payment pricing – a pricing tactic that breaks up the total price into smaller amounts payable over time Decoy pricing – a pricing strategy where a seller offers at least three similar products; two have comparable but more expensive prices and one of these two is less attractive to biers, thus causing more buyers to but the higher priced more attractive item Price bundling – selling two or more goods or services as a single package for one price Captive pricing – a pricing tactic for two items that must be used together; one item is priced very low and the firm makes its profit on another, high-margin item essential to the operation of the first item FOB origin pricing – a pricing tactic in which the cost of transporting the product from the factory to the customer’s location is the responsibility of the customer FOB delivered pricing – a pricing tactic in which the cost of loading and transporting the product to the customer is included in the selling price and is paid by the manufacturer Uniform delivered pricing – a pricing tactic in which a firm adds a standard shipping charge to the price for all customers regardless of location Freight absorption pricing – a pricing tactic in which the seller absorbs the total cost of transportation Trade discounts – discounts off list price of products to members of the cannel of distribution who perform various marketing functions Quantity discounts – a pricing tactic of charging reduced prices for purchases of larger quantities of a product Cash discounts – a discount offered to a customer to entice them too pay their bill quickly Seasonal discounts – price reductions offered only during certain times of the year Dynamic pricing – a pricing strategy in which the price can easily be adjusted to meet changes in the marketplace Internet price discrimination – an internet pricing strategy that changes different prices to different customers for the same product Online auctions – e-commerce that allows shoppers to purchase products through online bidding Freemium pricing – a business strategy in which a product in its most basic version is provided free of charge bit the company charges money (the premium) for upgraded versions of the product with more features, greater functionality, or greater capacity Internal reference price – a set price or a price range in consumers’ minds that they refer to in evaluating a product’s price Price lining – the practice of setting a limited number of different specific prices, called price points, for items in a product line Prestige pricing – (premium pricing); a pricing strategy used by luxury goods markets in which they keep the price artificially high to maintain a favorable image of the product Bait-and-switch – an illegal marketing practice in which an advertised price special is used as bait to get customers into the store with the intention of switching them to a higher-priced item Loss-leader pricing – the pricing policy of setting price very low or even below cost to attract customers into a store Unfair sales acts – state laws that prohibit suppliers from selling products below cost to protect small businesses from larger competitors Price fixing – the collaboration of two or more firms in setting prices, usually to keep prices high Predatory pricing – an illegal pricing strategy in which a company sets a very low price for the purpose of driving competitors out of business [Show More]

Last updated: 1 year ago

Preview 1 out of 8 pages

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

May 16, 2021

Number of pages

8

Written in

Additional information

This document has been written for:

Uploaded

May 16, 2021

Downloads

0

Views

35

(4).png)

.png)