Economics > EXAM > ECO 2301 Microeconomics Final Exam Review – Texas Tech University | ECO2301 Microeconomics Final E (All)

ECO 2301 Microeconomics Final Exam Review – Texas Tech University | ECO2301 Microeconomics Final Exam Review

Document Content and Description Below

ECO 2301 Microeconomics Final Exam Review – Texas Tech University Microeconomics Final Exam Review Chapter 1: Economics: Foundations and Models Definitions • Scarcity – The situa... tion in which unlimited wants exceed the limited resources available to fulfill those wants. • Economics – The study of the choices people make to attain their goals, given their scarce resources. • Economic Model – A simplified version of reality used to analyze real world economic situations. • Market – A group of buyers and sellers of a good or service and the institution or arrangement by which they come together to trade. • Marginal Analysis – Analysis that involves comparing marginal benefits and marginal costs • Trade-off – The idea that because of scarcity, producing more of one good or service means producing less of another good or service • Opportunity Cost – The highest-valued alternative that must be given up to engage in an activity • Centrally Planned Economy – An economy in which the government decides how economic resources will be allocated • Market Economy – An economy in which the decisions of households and firms interacting in markets allocate economic resources • Mixed Economy – An economy in which most economic decisions result from the interaction of buyers and sellers in markets but in which the government plays a significant role in the allocation of resources • Productive Efficiency – The situation in which a good or service is produced at the lowest possible cost • Allocative Efficiency – A state of the economy in which production is in accordance with consumer preferences; in particular, every good or service is produced up to the point where the last unit provides a marginal benefit to society equal to the marginal cost of producing it • Voluntary Exchange – The situation that occurs in markets when both the buyer and seller of a product are made better off by the transaction • Equity – The fair distribution of economic benefits • Economic Variable – Something measurable that can have different values, such as the wages of software programmers • Positive Analysis – Analysis concerned with what is • Normative Analysis – Analysis concerned with what ought to be • Microeconomics – The study of how households and firms make choices, how they interact in markets, and how the government attempts to influence their choices • Macroeconomics – The study of the economy as a whole, including topics such as inflation, unemployment, and economic growth Review Questions 1. A primary difference between macroeconomics and microeconomics is a. There are no true differences between microeconomics and macroeconomics. b. Microeconomics is concerned with market economies while macroeconomics is concerned with centrally- planned economies. c. Microeconomics examines individual markets while macroeconomics examines the economy as a whole. d. Microeconomics is concerned with present decisions while macroeconomics is concerned with future decisions. 2. Economists use models: a. To answer questions and analyze issues. b. To describe the real world exactly. c. To disprove economic data. d. To prove that theories are true. 3. Economic data is used: a. Only if all relevant data is available. b. To take the place of an economic model. c. To prove that a model is true. d. To test models. 4. Economists assume that people are rational in the sense that: a. They make decisions based on total, rather than marginal, variables. b. The do not respond to economic incentives. c. They use all available information as they take actions intended to achieve their goals. d. They generally make the correct choices. 5. Which of the following is not a step that economists use in developing a successful economic model? a. Use economic data to test the hypothesis. b. Make a value judgment about the merits of the hypothesis. c. Formulate a testable hypothesis. d. Revise the model if it does not explain the data well. e. Decide on the assumptions to be used in developing the model. 6. Which of the following covers the study of topics such as inflation or unemployment? a. Microeconomics b. Macroeconomics c. Both microeconomics and microeconomics give equal emphasis to these problems. d. None of the above 7. What type of economic analysis is concerned with the way things ought to be? a. Rational Behavior b. Normative Analysis c. Marginal Analysis d. Positive Analysis 8. Productive efficiency means that a. A good or service is produced as quickly as possible. b. Every good or service is produced up to the point where marginal benefit is equal to marginal cost. c. Every good or service is distributed fairly. d. A good or service is produced at the lowest possible cost. 9. Allocative efficiency means that a. A good or service is produced as quickly as possible. b. A good or service is produced at the lowest possible cost. c. Every good or service is distributed fairly. d. Every good or service is produced up to the point where marginal benefit is equal to marginal cost. 10. Which of the following best describes scarcity? a. Prices of goods are very high. b. Markets cannot properly allocate resources. c. Wants cannot be fulfilled and thus all goods must be rationed. d. Unlimited wants exceed the limited resources available. 11. Scarcity is central to the study of economics because it implies that a. Society must make decisions at the margin. b. Economic agents are rational. c. Wants are unlimited. d. Every choice involves an opportunity cost. 12. The three economic questions that every society must answer are a. What goods will be produced, how will they be produced, and who will receive the goods? b. What kind of government will the society have, how will it run, and who will run it? c. What are the prices of goods, how are they determined, and who will pay them? d. What economic system will be used, how will it be implemented, and who will make market decisions? 13. Centrally planned economies allocate resources based on decisions by __________, while market economies answer these questions through decisions made by ___________. 14. Efficiency means that goods are distributed in a way that ____________________, while equity means that goods are distributed in a way that ____________. 15. What goods and services will be produced, how the goods and services will be produced, and who will receive the goods and services are determined: a. In centrally planned economies by the government. b. In market economies by the decisions of households and firms interacting in markets. c. In centrally planned economies partly by the decisions of buyers and sellers interacting in markets and partly by the government. d. In mixed economies by the government. e. Both A and B are true. 16. Economics assumes people and firms: a. Know everything, respond to incentives, and make decisions by comparing marginal benefits with marginal costs. b. Use all available information to achieve their goals, respond to incentives, and make decisions by continuing any activity up to the point where marginal benefit equals zero. c. Are rational, respond to incentives, and make all-or-nothing decisions. d. Use all available information to achieve their goals, respond to incentives, and make decisions by comparing total benefits with total costs. e. Are rational, respond to incentives, and make decisions by comparing marginal benefits with marginal costs. 17. A portion of microeconomics examines: a. The economy as a whole, such as why some economies have grown faster than others. b. How individual firms make choices, such as how they decide what prices to charge. c. Policy issues, such as whether government intervention can reduce the severity of recessions. d. The economy as a whole, such as what causes unemployment. e. All of the above. 18. Macroeconomics examines: a. How individual households make choices, such as how they react to changes in product prices. - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - d. Price floors because, when non-binding, price floors increase price above the equilibrium and may increase producer surplus. e. Price floors because, when binding, price floors increase price above the equilibrium and increase economic efficiency. 12. Producer surplus is: a. The difference between the lowest price a firm would be willing to accept and marginal cost. b. The difference between the lowest price a firm would be willing to accept and the price it actually receives. c. The difference between the highest price a consumer is willing to pay and the lowest price a firm would be willing to accept. d. The difference between the highest price a consumer is willing to pay and the price the consumer actually pays. e. The market price multiplied by the number of units sold by a firm. 13. How does producer surplus change as the equilibrium price of a good rises or falls? As the price of a good rises, producer surplus ______, and as the price of a good falls, producer surplus _______. 14. Economic efficiency: a. Is a market outcome in which the sum of consumer surplus and producer surplus is at a maximum. b. Is a market outcome in which the marginal benefit to consumers of the last unit produced is equal to its marginal cost of production. c. Is a market outcome in which every individual is better off than they would be at any other market outcome. d. Both A and B. e. All of the above. 15. Economists define economic efficiency in this way: a. To help policymakers understand the negative consequences of price floors. b. To help policymakers understand the negative consequences of price ceilings. c. To help policymakers understand the negative consequences of taxes. d. To illustrate the benefits of a competitive market equilibrium. e. All of the above. 16. Tax incidence indicates: a. Who is legally required to send a tax payment to the government. b. The burden of a tax on producers. c. The actual division of the burden of a tax. d. Who is not legally required to send a tax payment to the government. e. The burden of a tax on consumers. 17. Do the people who are legally required to pay a tax always bear the burden of the tax? Briefly explain. a. No. Whoever bears the burden of the tax is not affected by who legally is required to pay the tax to the government. b. No. Consumers always bear the burden of the tax. c. No. Producers always bear the burden of the tax. d. Yes. Those who are legally required to send a tax payment to the government bear the burden of the tax. e. No. Those who are legally required to send a tax payment to the government never bear the burden of the tax. 18. Marginal benefit is: a. The enjoyment people receive from consuming a product. b. A legally determined maximum price that sellers may charge. c. The difference between the highest price a consumer is willing to pay and the price the consumer actually pays. d. The additional benefit from consuming one more unit. e. The additional cost of producing one more unit. 19. Why is the demand curve referred to as a marginal benefit curve? a. It shows the price consumers actually pay to consume a product. b. It shows the difference between the highest price a consumer is willing to pay and the marginal benefit of consumption. c. It shows the willingness of firms to supply a product at different prices. d. It shows the willingness of consumers to purchase a product at different prices. e. It shows the difference between the highest price a consumer is willing to pay and the lowest price a firm would be willing to accept. 20. Does it matter whether buyers or sellers are legally responsible for paying a tax? a. No, the market price to consumers and net proceeds to sellers are the same independent of who pays the tax. b. Yes, the tax is more equitable if sellers pay the tax. c. Yes, the tax is more efficient if consumers pay the tax. 21. Consider the market for gasoline illustrated in the figure below. Suppose the market is perfectly competitive and initially in equilibrium. Now suppose the government imposes a gasoline tax of $1.50 to be paid for by producers. The effect of this tax is illustrated in the figure. Who bears the burden of the tax? Consumers pay $____ of the $1.50 tax and producers pay $____ of the tax. 22. Consider the market for wheat, depicted in the figure below. Suppose a price floor of p3 is imposed by the government. As a result of the price floor, there is a ______ (shortage or surplus) of wheat. Compared with the market-clearing equilibrium, is the price floor efficient? ______ What area represents the loss in efficiency in terms of consumer and producer surplus resulting from the price floor? Shade in deadweight loss. 23. Consider the market for Apple iPods. Assume the market is perfectly competitive and at a market-clearing equilibrium. What area represents consumer surplus? What area represents producer surplus? 24. Consider the market for sugar illustrated in the figure below. Suppose the market is perfectly competitive and initially in equilibrium at a price of p2 and a quantity of Q2. Now suppose the government applies a price floor of p3. Compared with the market-clearing equilibrium, consumer surplus would a. Decrease by area B b. Decrease by area E c. Decrease by areas B and F d. Increase by area C e. Decrease by areas B and E In turn, producer surplus would a. Increase by area B and decrease by area F b. Increase by area B c. Increase by areas B and E d. Decrease by area C e. Increase by areas B, E, and G Consequently, with the price floor, deadweight loss would equal a. No areas b. Areas B, C, E, and F c. Areas E and F d. Area E e. Area F 25. Consider the market for eggs illustrated in the figure below. Suppose the market is perfectly competitive and initially in equilibrium at a price of 5 cents and a quantity of 50 (thousand). If the price were 7 cents instead of 5 cents, then consumer surplus would a. Increase by area C b. Decrease by area B c. Increase by areas C and F d. Decrease by areas B and F e. Decrease by areas B and E In turn, producer surplus would a. Increase by area B b. Increase by areas C and F c. Increase by areas B and E d. Decrease by area C e. Increase by area B and decrease by area F Consequently, at a price of 7 cents, deadweight loss would equal a. Area E b. Areas E and F c. No areas d. Area F e. Areas B, C, E, and F 26. The graph below shows the market demand and supply for eggs. Assume that the market for eggs is perfectly competitive. Suppose the egg producers organize themselves and establish a system of quotas. Each farmer’s output is restricted by an amount indicated in the graph. Compared with the market-clearing equilibrium, is the quota system efficient? _____ Illustrate the loss of efficiency that results from the quota system by shading in deadweight loss. 27. Tim mows neighborhood lawns for extra money. Suppose that he would be willing to mow one lawn for $14, a second lawn for $16, and a third lawn for $25. Also suppose that three neighbors are interested in having their lawns mowed. Mrs. Jones would be willing to pay $35 to have her lawn mowed, Mr. Wilson would be willing to pay $26, and Ms. Smith would be willing to pay $25. If Tim offers to mow lawns for $25 each, what will be his producer surplus? $_____. Considering Mrs. Jones, Mr. Wilson, and Ms. Smith together, what will be their consumer surplus? $_____. 28. Consider the market for gasoline illustrated in the figure below. Suppose the market is perfectly competitive and initially in equilibrium. Now suppose the government imposes a gasoline tax of $2.00 to be paid for by consumers. Show how the tax affects the market for gasoline. Add either a new supply or demand curve. How much government revenue does the gasoline tax generate? $_____. What effect does the gasoline tax have on efficiency (relative to the no-tax equilibrium)? a. The tax has no effect on efficiency. Instead, surplus is simply transferred from customers and producers to the government. b. The tax increases efficiency by raising new government revenue. c. The tax decreases efficiency because consumer and producer surplus decrease by more than government revenue increases. d. The tax increases efficiency because consumer and producer surplus decrease by less than government revenue increases. e. The tax decreases efficiency because consumer and producer surplus decrease by less than government revenue increases. Chapter 2: Trade-offs, Comparative Advantage, and the Market System Definitions • Production Possibilities Frontier (PPF) – A curve showing the maximum attainable combinations of two products that may be produced with available resources and current technology. • Economic growth – The ability of the economy to produce increasing quantities of goods and services. • Trade – The act of buying or selling. • Absolute Advantage – The ability of an individual, a firm, or a country to produce more of a good or service than competitors, using the same amount of resources. • Comparative Advantage – The ability of an individual, a firm, or a country to produce a good or service at a lower opportunity cost than competitors. • Market – A group of buyers and sellers of a good or service and the institution or arrangement by which they come together to trade. • Product Markets – Markets for goods – such as computers – and services – such as medical treatment. • Factor Markets – Markets for the factors of production, such as labor, capital, natural resources, and entrepreneurial ability. • Factors of Production – The inputs used to make goods and services. (Labor, Capital, Natural Resources & Entrepreneurial Ability) • Circular-Flow Diagram – A model that illustrates how participants in markets are linked. • Free Market – A market with few government restrictions on how a good or service can be produced or sold or on how a factor of production can be employed. • Entrepreneur – Someone who operates a business, bringing together the factors of production – labor, capital, and natural resources – to produce goods and services. • Property Rights – The rights individuals or firms have to the exclusive use of their property, including the right to buy or sell it. Review Questions 1. What is a free market? a. A free market is one where the government restricts how a good or service can be produced. b. A free market is one where the government does not control the production of goods and services. c. A free market is one where the government restricts how a factor of production can be employed. d. A free market is one with perfect equality. e. A free market is one without property rights. 2. In what ways does a free market economy differ from a centrally planned economy? Unlike a free market economy, a. Centrally planned economies do not trade internationally. b. Centrally planned economies do not use money. c. Centrally planned economies have no government restrictions. d. Centrally planned economies have no government. e. Centrally planned economies have extensive government controls. 3. What does increasing marginal opportunity costs mean? a. Increasing the production of a good requires decreases in the production of another good. b. Increasing the production of a good requires larger and larger decreases in the production of another good. c. The economy is unable to produce increasing quantities of goods and services. - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - c. When the marginal cost of the last unit produced is below the average, it pulls the average down, and when the marginal cost is above the average, it pulls the average up. d. The firm begins experiencing diminishing returns at this quantity. e. The firm begins experiencing economies of scale at this quantity. 13. If the marginal product of labor is falling, is the marginal cost of production rising or falling? If the additional output from each new worker is falling, a. The marginal cost of that output is rising due to diseconomies of scale. b. The marginal cost of that output is rising due to division of labor. c. The marginal cost of that output is rising because the total cost of labor is increasing with each additional worker. d. The marginal cost of that output is rising because the only additional cost to producing more output is the additional wages paid to hire more workers. e. The marginal cost of that output is falling because the only additional cost to producing more output is the additional wages paid to hire more workers. 14. Is it possible for technological change to be negative? If so, give an example. a. It is possible for technological change to be negative. An example is when a firm hires less-skilled workers. b. It is possible for technological change to be negative. An example is when a firm installs more reliable equipment. c. No. Technological change is neither positive nor negative because it refers to a process. d. No. Technological change is always positive because it refers to the development of new products. e. It is possible for technological change to be negative. An example is when a firm installs faster machinery. 15. Minimum efficient scale is a. The level of output at which the long-run average cost of production begins to decline. b. The level of output at which a firm begins to experience economies of scale. c. The level of output at which the marginal cost of production reaches a minimum. d. The level of output at which all diseconomies of scale are exhausted. e. The level of output at which all economies of scale are exhausted. 16. What is likely to happen in the long run to firms that do not reach minimum efficient scale? A firm that does not reach its minimum efficient scale a. Will lose money if it remains in business. b. Will be better off going out of business. c. Will become a natural monopoly. d. Will earn positive profits if it remains in business. e. Both A and B. 17. Suppose Anna hires workers to cook pizzas. If the first worker’s marginal product is 22 pizzas, the second worker’s marginal product is 35, and the third worker’s marginal product is 32, then the average product of labor is ____ pizzas. Now suppose Anna hires a fourth worker whose marginal product is below the average. If so, then the average product of labor will _______. 18. An example of technological change is a. A firm rearranging the factory floor to increase production. b. A firm’s workers going through a training program. c. A hurricane damaging firm facilities. d. Both A and B. e. All of the above. 19. Consider the production of hamburgers. The average total cost and average variable cost of producing hamburgers are illustrated in the graph. Graph the marginal cost of producing hamburgers. 20. Suppose Sheri owns a restaurant that serves pizza using three inputs: workers, restaurant space (and layout), and ovens. If workers are variable, restaurant space (and layout) is variable, and ovens are variable, then Sheri is producing pizza in the ___________. (Long Run or Short Run) 21. Books can be produced using either a small or large bookstore. The graph shows the average total cost of producing books using a small bookstore (ATCS) and a large bookstore (ATCL). Suppose Parker plans on selling 600 books. If so, then Parker should choose to produce a ______ (small or large) bookstore, where the average total cost of production is $____. 22. Consider the production of hotdogs. Given the average total cost of producing hotdogs illustrated in the graph, which of the following is true of the marginal cost of producing hotdogs? a. The marginal cost of producing up to 400 hotdogs is less than the average total cost, but the marginal cost of producing more than 400 hotdogs is greater than the average total cost. b. The marginal cost of production is exactly equal to the average total cost at 400 hotdogs. c. The marginal cost of producing up to 400 hotdogs is decreasing, but the marginal cost of producing more than 400 hotdogs is increasing. d. The marginal cost of production is always greater than the average total cost. e. Both A and B. 23. What is the distinction between the economic short run and the economic long run? a. In the short run, the firm incurs only fixed costs, but in the long run, the firm incurs fixed and variable costs. b. In the short run, the firm incurs explicit and implicit costs, but in the long run, the firm incurs only explicit costs. c. In the short run, at least one input is fixed, but in the long run, the firm can vary all inputs. d. In the short run, the firm incurs some opportunity costs, but in the long run, the firm incurs no opportunity costs. e. In the short run, the firm can vary all inputs, but in the long run, at least one input is fixed. 24. Suppose Miles hires workers to cook hotdogs. The table below shows how many hotdogs can be produced with various quantities of labor. Calculate the marginal product of labor. When the marginal product of labor is decreasing, the average product of labor is _______ (greater/less than) the marginal product of labor, and when the marginal product of labor is increasing, the average product of labor is ______ (greater/less than) the marginal product of labor. 25. In economics, the best definition of technology is a. The process a firm uses to price output. b. The sophistication of the equipment enjoyed by consumers. c. The speed of communication. d. The development of new products. e. The process a firm uses to turn inputs into outputs. 26. Further, positive technological change is defined as a. Being able to produce more output using the same inputs. b. Being able to produce the same output using fewer inputs. c. Being able to sell more output at higher prices. d. Both A and B. e. All of the above. 27. Consider the production of hamburgers. The average total cost and average fixed cost of producing hamburgers are illustrated in the graph below. Graph the average variable cost of producing one, two, three, and four thousand hamburgers. 28. Andrew owns a restaurant that sells pizzas. The long run average cost of selling pizzas is illustrated in the graph. Suppose Andrew is currently selling 600 pizzas. In the long run, Andrew should ______ (reduce or expand) output to reduce the long run average cost of production. Specifically, to sell on the minimum efficient scale in the long run, Andrew should expand output to ____ pizzas. 29. Suppose Susan is currently producing 100,000 hamburgers per month at a total cost of $20,000.00. What is her average total cost of production? $_____ Now suppose Susan increases production to 100,001 hamburgers, and the total cost of production increases to $20,000.08. What is her marginal cost of producing the 100,001th hamburger? $_____ Since the marginal cost of production is less than the average cost of production, the average total cost of production must be ________ (falling or rising). Chapter 11: Firms in Perfectly Competitive Markets Definitions • Perfectly competitive market – A market that meets the conditions of (1) many buyers and sellers, (2) all firms selling identical products, and (3) no barriers to new firms entering the market. • Price taker – a buyer or seller that is unable to affect the market price. • Profit – Total revenue minus total cost. • Average revenue (AR) – Total revenue divided by the quantity of the product sold. • Marginal revenue (MR) – Change in total revenue from selling one more unit of a product. • Sunk cost – A cost that has already been paid and that cannot be recovered. [Show More]

Last updated: 1 year ago

Preview 1 out of 208 pages

Reviews( 0 )

Recommended For You

Business> EXAM > Principles of Microeconomics Final Exam | 68 Questions with 100% Correct Answers (All)

Principles of Microeconomics Final Exam | 68 Questions with 100% Correct Answers

When a tax is imposed on the buyers of a good, the demand curve shifts - ✔✔downward by the amount of the tax Efficiency is attained when - ✔✔total surplus is maximized. The size of the deadweight l...

By Tessa , Uploaded: Aug 09, 2022

$5

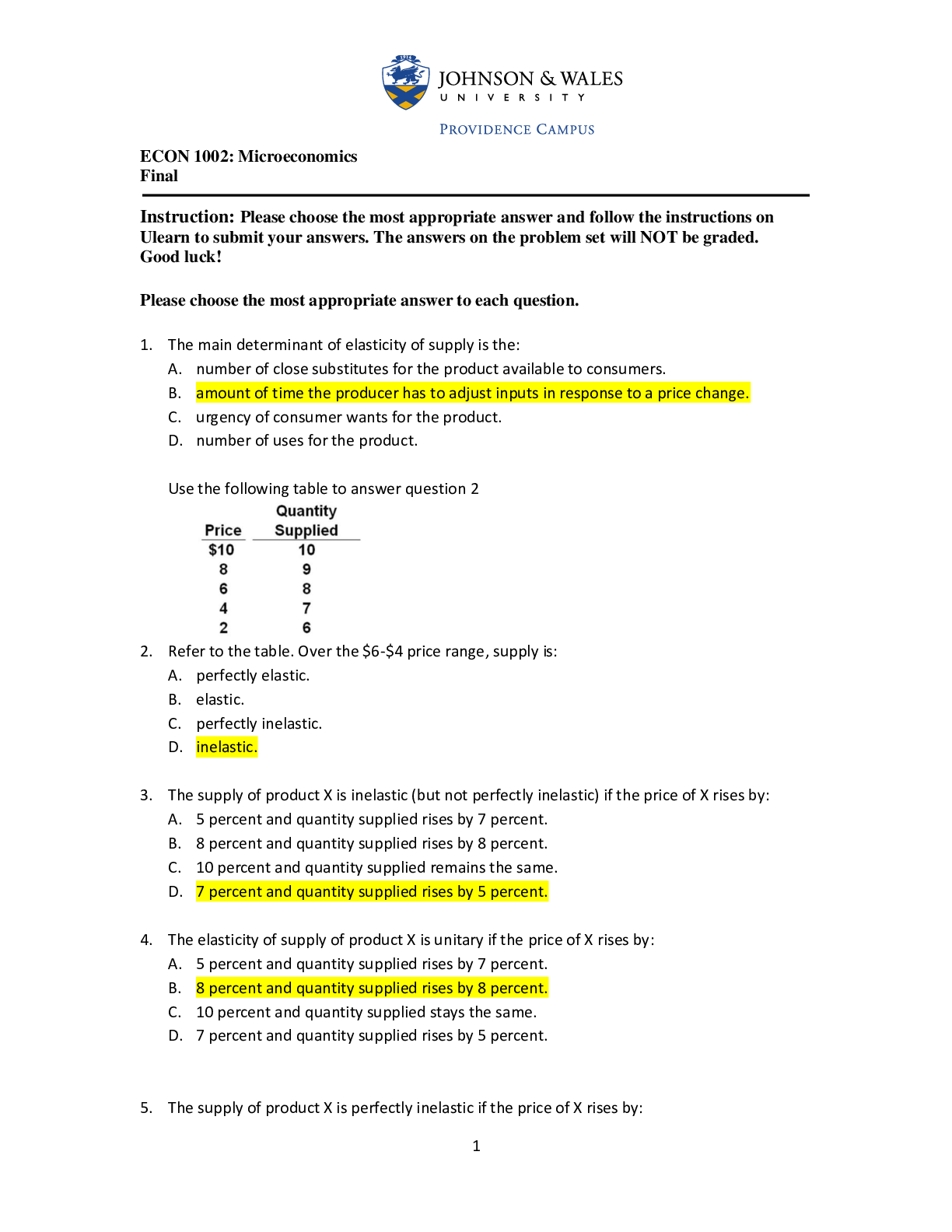

Macroeconomics> EXAM > ECON 1002: Microeconomics Final Exam (3) Complete Answers (spring 2020). (All)

ECON 1002: Microeconomics Final Exam (3) Complete Answers (spring 2020).

ECON 1002: Microeconomics Final 1. The main determinant of elasticity of supply is the: A. number of close substitutes for the product available to consumers. B. amount of time the producer...

By Expert1 , Uploaded: Aug 12, 2020

$17

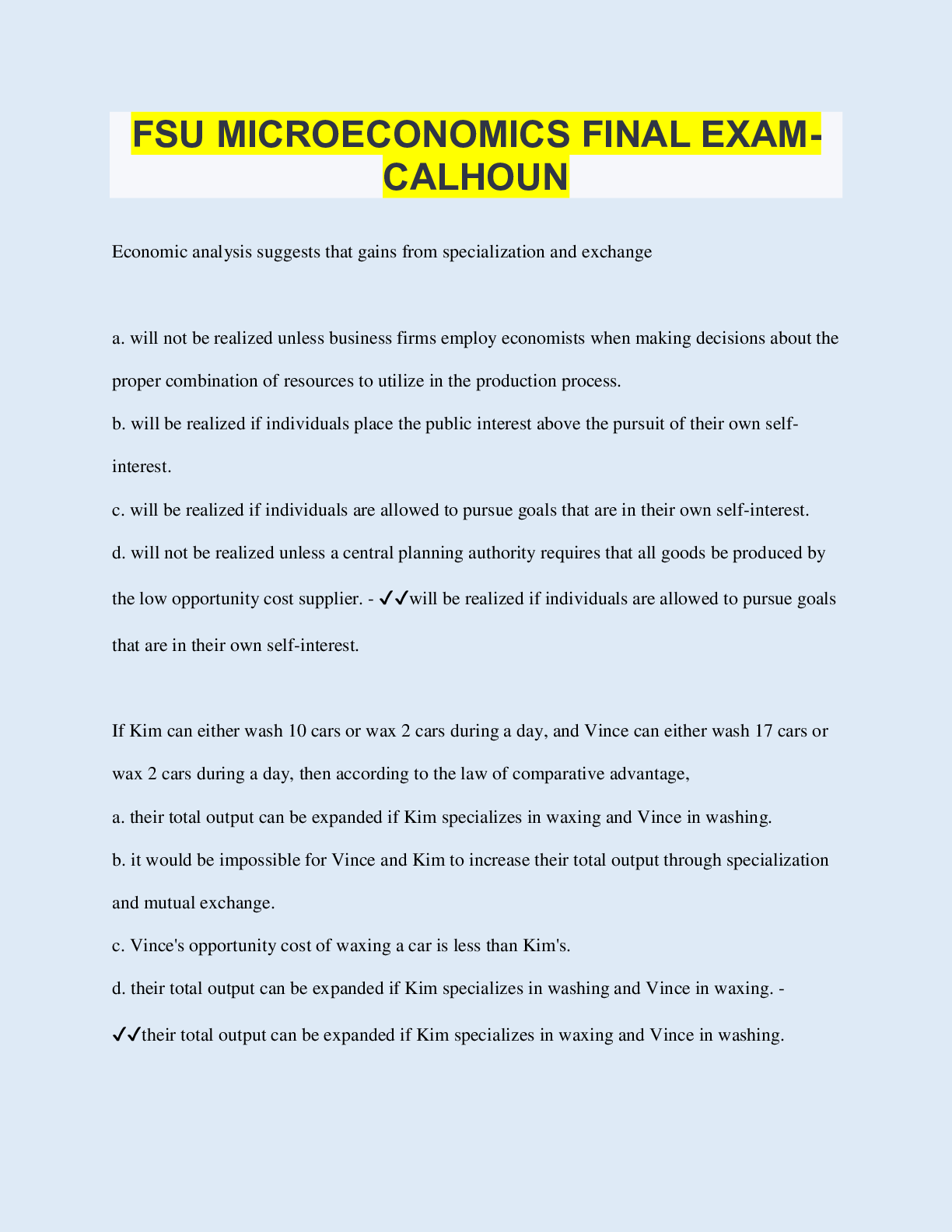

Economics> EXAM > FSU MICROECONOMICS FINAL EXAM- CALHOUN | 75 Questions with 100% Correct Answers | Updated 2023 | 29 Pages (All)

FSU MICROECONOMICS FINAL EXAM- CALHOUN | 75 Questions with 100% Correct Answers | Updated 2023 | 29 Pages

Economic analysis suggests that gains from specialization and exchange a. will not be realized unless business firms employ economists when making decisions about the proper combination of resources...

By Toya , Uploaded: Jan 19, 2023

$15

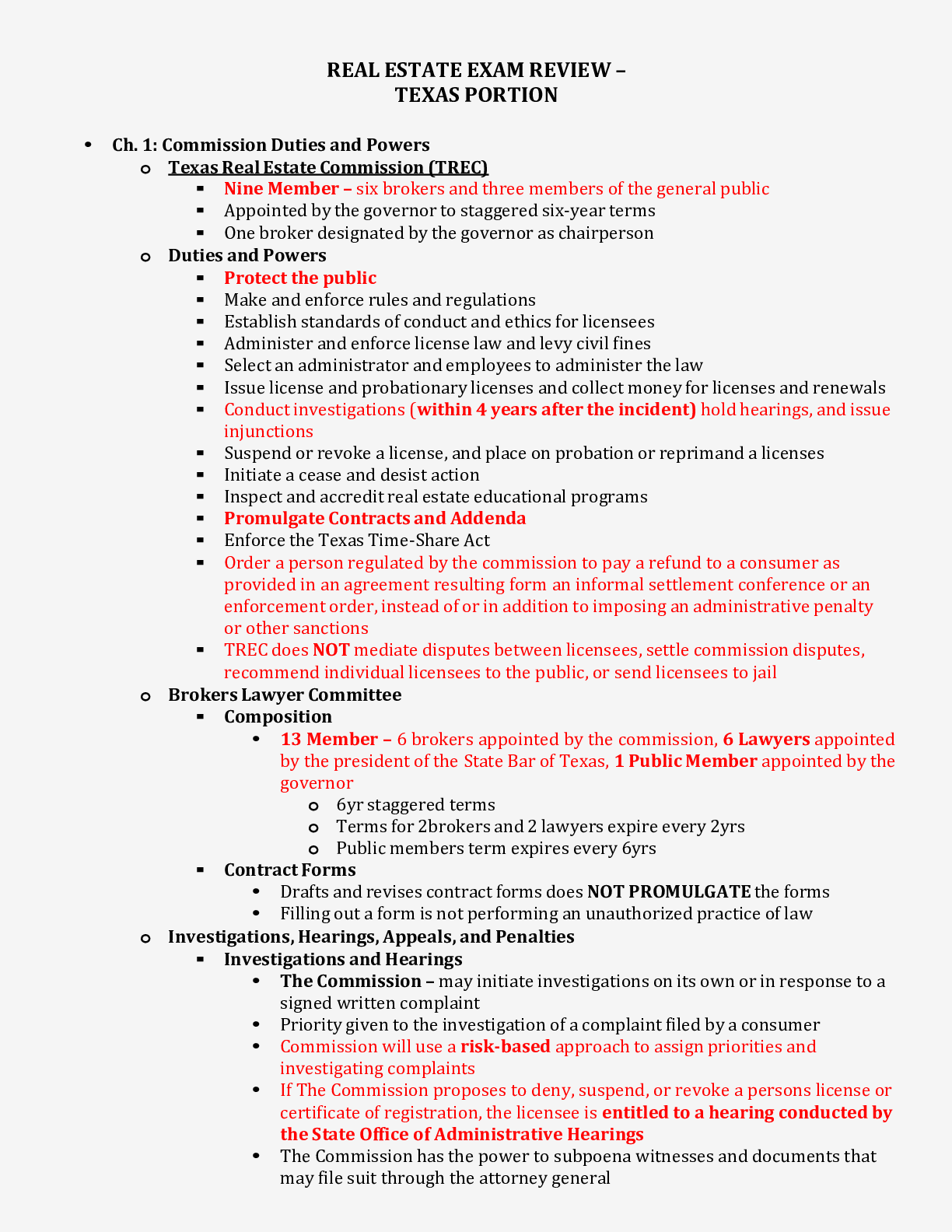

Accounting> EXAM > REAL ESTATE EXAM REVIEW – TEXAS PORTION (All)

REAL ESTATE EXAM REVIEW – TEXAS PORTION

REAL ESTATE EXAM REVIEW – TEXAS PORTION

By BESTGRADE01 , Uploaded: Oct 19, 2023

$10

*NURSING> EXAM > NGR 6172 Pharm Midterm Exam- Questions and Answers. Score 98% (All)

NGR 6172 Pharm Midterm Exam- Questions and Answers. Score 98%

NGR 6172 Pharm Midterm Exam- Questions and Answers GRADED A-1). A patient who takes daily doses of aspirin is scheduled for surgery next week. The nurse should advise the patient to: a. continue to...

By PROF , Uploaded: Feb 01, 2022

$11

Philosophy> EXAM > PHL 200 Intro to Ethics Unit 3 - Score 100% (All)

PHL 200 Intro to Ethics Unit 3 - Score 100%

PHL 200 Intro to Ethics Unit 3 For a utilitarian, which consideration is most important? Why is utilitarianism an objectivist or relativist theory? Which of the following considerations is important f...

By Ajay25 , Uploaded: Jan 04, 2022

$8

Philosophy> EXAM > PHL 200 Intro to Ethics Unit 2 -Score 100% (All)

PHL 200 Intro to Ethics Unit 2 -Score 100%

PHL 200 Intro to Ethics Unit 2 Which of the following statements about divine command theory is true? Norman learns from his pastor that God commands people to love one another. Thus according to divi...

By Ajay25 , Uploaded: Jan 04, 2022

$8

Philosophy> EXAM > PHL 200 Intro to Ethics Unit Final. Score 100% (All)

PHL 200 Intro to Ethics Unit Final. Score 100%

PHL 200 Intro to Ethics Unit Final Which of the following statements supports egoism? "Abortion is acceptable if the woman doesn't want to be a mother." To which theory of ethics is the person who mad...

By Ajay25 , Uploaded: Jan 04, 2022

$8

Philosophy> EXAM > Intro to Ethics PHL 200 Unit 1 - Questions and Answers (All)

Intro to Ethics PHL 200 Unit 1 - Questions and Answers

PHL 200 Intro to Ethics Unit 1 Which of the following statements best describes the relationship between philosophy and science? Which of the following is a philosophical question? Which of the follow...

By Ajay25 , Uploaded: Jan 04, 2022

$9

Philosophy> EXAM > PHL 200 Introduction to Ethics Unit 4 - Questions and Answers (All)

PHL 200 Introduction to Ethics Unit 4 - Questions and Answers

PHL 200 Intro to Ethics Unit 4 Which of the following best defines virtue-based ethics? Choose the true statement about virtue-based ethics. Jean lies to her boss about not feeling well so she can sta...

By Ajay25 , Uploaded: Jan 04, 2022

$10

Document information

Connected school, study & course

About the document

Uploaded On

Oct 14, 2020

Number of pages

208

Written in

Additional information

This document has been written for:

Uploaded

Oct 14, 2020

Downloads

0

Views

318